Biomethane in EU Gas Grids: Overview of member states and the five largest markets

For the SAF platform, we have prepared a review of the report “How costs to connect biomethane to gas grids are paid for”, conducted by Common Futures for the European Biogas Association (EBA).

The aim of this study was to examine how the costs of integrating biomethane into the gas grid are allocated between producers and infrastructure companies across EU countries. The research disaggregates infrastructure-related investments into individual cost components and analyzes each in detail.

EU Member States Overview

The EU has over 2 million kilometers of gas distribution pipelines. Their large extent and low operating pressure explain why the majority of biomethane plants (58%) are connected to distribution grids.

The EU’s transmission network spans over 260,000 km, enabling long-distance transport of methane to major industries and storage sites.

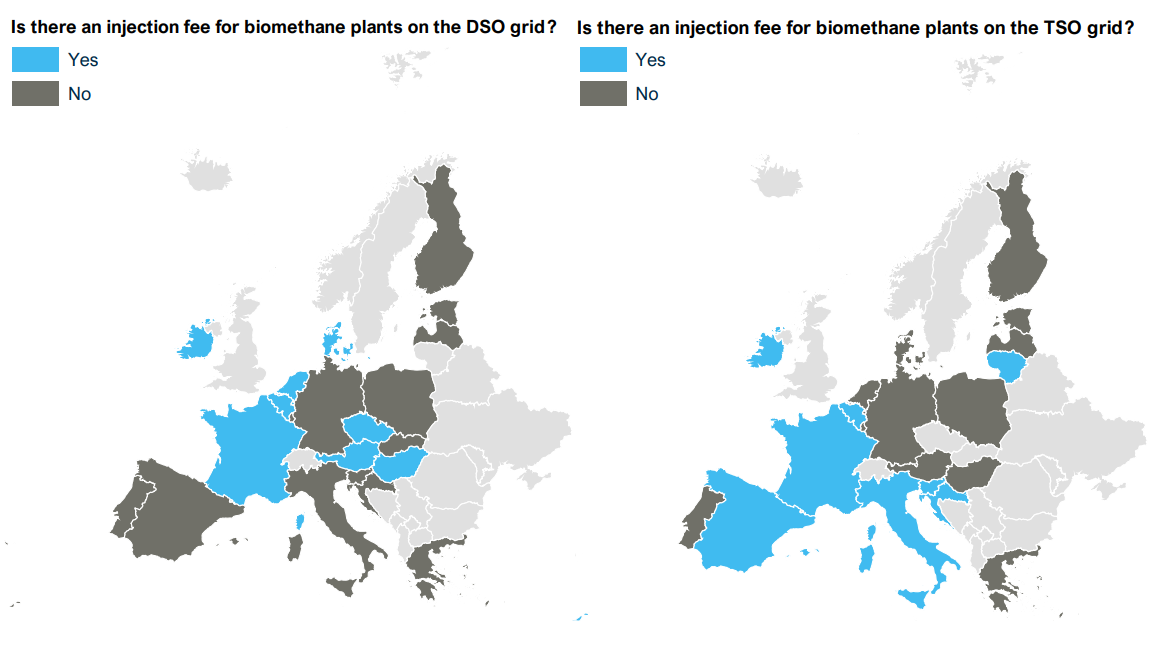

There is no harmonized approach to injection fees. Some countries waive them for biomethane producers, while others — including both mature and emerging markets — impose such fees. In total, 9 distribution system operators and 8 transmission system operators in the EU currently charge injection fees.

Key Findings

Around 60% of biomethane plants in the EU are connected to distribution networks. Cost-sharing practices are more prevalent for distribution grid connections, largely due to broader experience across Member States. In contrast, transmission grid connections involve less frequent cost-sharing, likely due to limited experience in this area.

The study breaks down each type of grid connection or upgrade into key components and outlines financial and operational responsibilities for each.

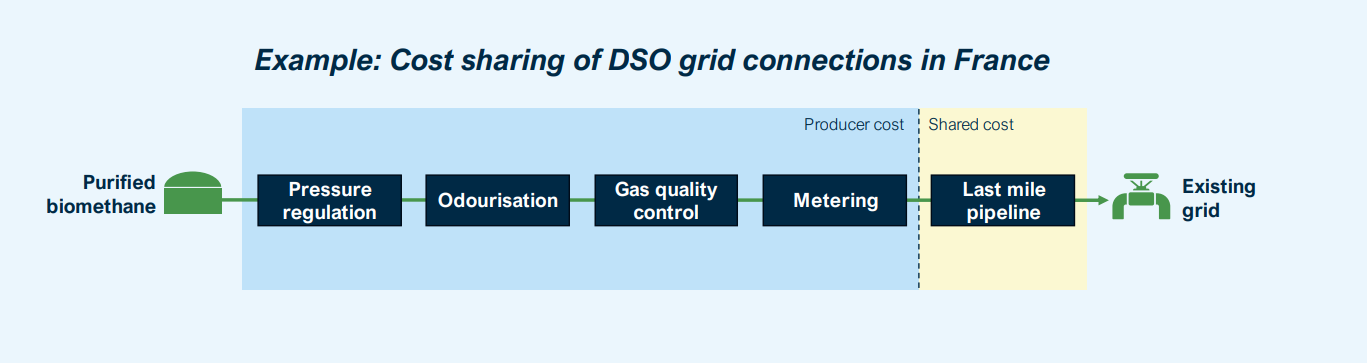

The following cost allocation methods were identified:

- Split between CAPEX and OPEX

E.g., Portugal – producer pays capital costs; DSO covers operational costs. - Regulated percentage share

E.g., Germany – grid operator covers 75% of the connection costs. - Component-level cost sharing

E.g., the “last mile” pipeline in the Netherlands is financed by the TSO.

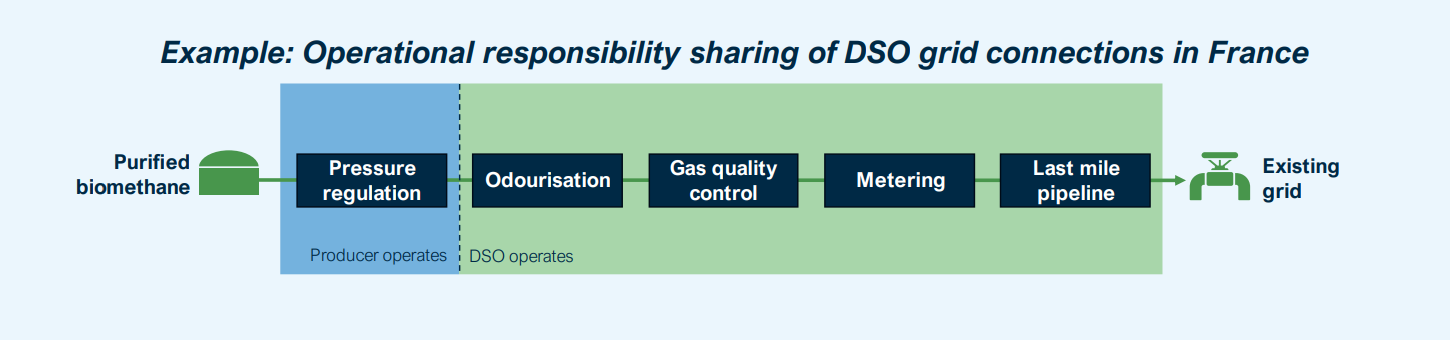

The study also examines the operational responsibility for each type of connection and component, as illustrated below using the example of connections to distribution networks in France.

Operational responsibility also varies across Member States. “Last mile” pipelines and odorization systems are typically handled by grid operators. Gas quality control and metering may be shared or vary, depending on national regulations. Pressure regulation usually falls under the producer’s scope — especially where compression is required.

Read the full material with a chapter on the five largest biomethane markets in the EU today on the SAF platform. You can also download the report there.

We remind you that UABIO is a partner of the Sustainable agribusiness platform (SAF).

SAF is a communication platform that brings together agribusiness stakeholders and aims to establish strong links between market players and introduce sustainable approaches in agriculture. For this platform, our team prepares verified professional content on the bioenergy sector.