Biomethane in Europe: Why scaling up is harder than it looks?

The European Union has set an ambitious goal: to become a global leader in biomethane production, seeing it as the key to energy independence and decarbonization. But is reality keeping pace with political declarations?

In January 2026, the Oxford Institute for Energy Studies (OIES) published a working paper titled “Biomethane in Europe: Why scaling up is harder than it looks” (OIES Paper: NG, No. 203).

The author of the study is Maria Olczak, a research fellow at OIES. In her work, she examines in detail why the ambitious goals of the REPowerEU plan currently seem unattainable, how the new FuelEU Maritime regulations are creating unexpected opportunities, and what fundamental differences in regulatory models are hindering the sector’s development.

Here are the key points of this work.

Growth and dependence on subsidies

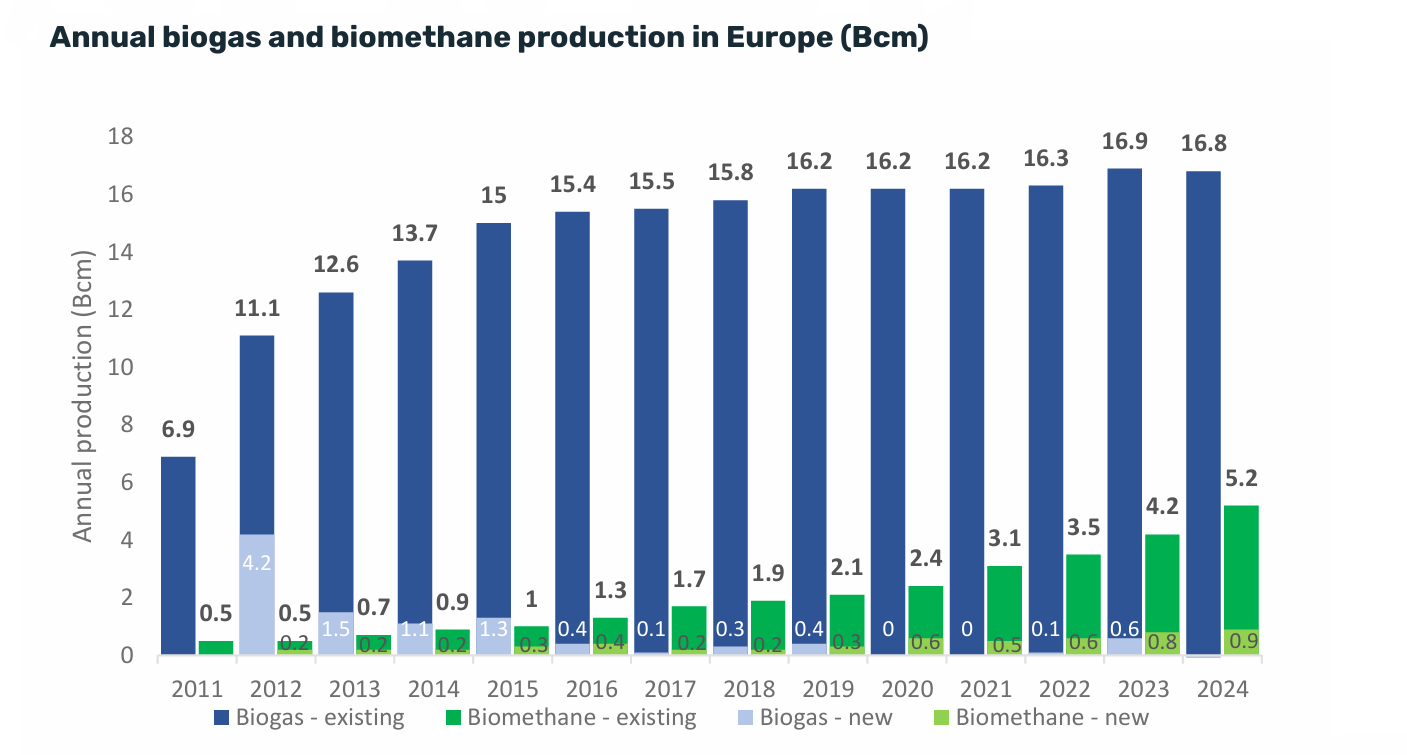

European production of biogas and biomethane increased by 34% between 2015 and 2024 — from 173 TWh to 232 TWh (22 billion cubic meters). Europe accounts for nearly half of global production. The share of biomethane alone grew by 24% in 2024 alone, reaching 52 TWh (5.2 billion cubic meters). As of mid-2025, there were 1,620 biomethane plants in operation in Europe.

France has overtaken Germany to become the EU’s largest producer of biomethane. At the same time, Germany remains the leader in total biogas and biomethane production. Ninety percent of production is concentrated in five member states and the United Kingdom.

Despite this growth, biomethane remains significantly more expensive than natural gas: production costs range from 50 to 175 euros/MWh, while the TTF price in 2025 is expected to be around 38 euros/MWh. No significant reduction in costs has been observed since the late 2010s, and even forecasts through 2050 do not anticipate price parity with natural gas.

Is the REPowerEU goal achievable?

In 2022, as part of the REPowerEU plan, the European Commission set a non-binding target of achieving 35 billion cubic meters of biomethane production per year by 2030. However, the national plans of member states project a combined production of biogas and biomethane of only about 26 billion cubic meters, of which pure biomethane accounts for just 12–15 billion cubic meters. This means the shortfall relative to the target is 20–23 billion cubic meters.

Interestingly, in its public communications from 2025, the European Commission is already referring to a target of 35 billion cubic meters “in the form of biogas or its processed version” — a departure from its original ambition to focus exclusively on biomethane. This may also indicate a reassessment of biogas’s role in the decarbonization strategy.

Transport as a new source of demand

The FuelEU Maritime Regulation, which took effect on January 1, 2025, requires large commercial vessels to gradually reduce the carbon intensity of their fuel by 2% by 2025 and by 80% by 2050. Liquefied biomethane (bio-LNG)—produced specifically from manure, which has a negative carbon footprint—is becoming an exciting solution. Its main advantages include low carbon intensity, compatibility with existing infrastructure, and lower cost compared to other alternatives.

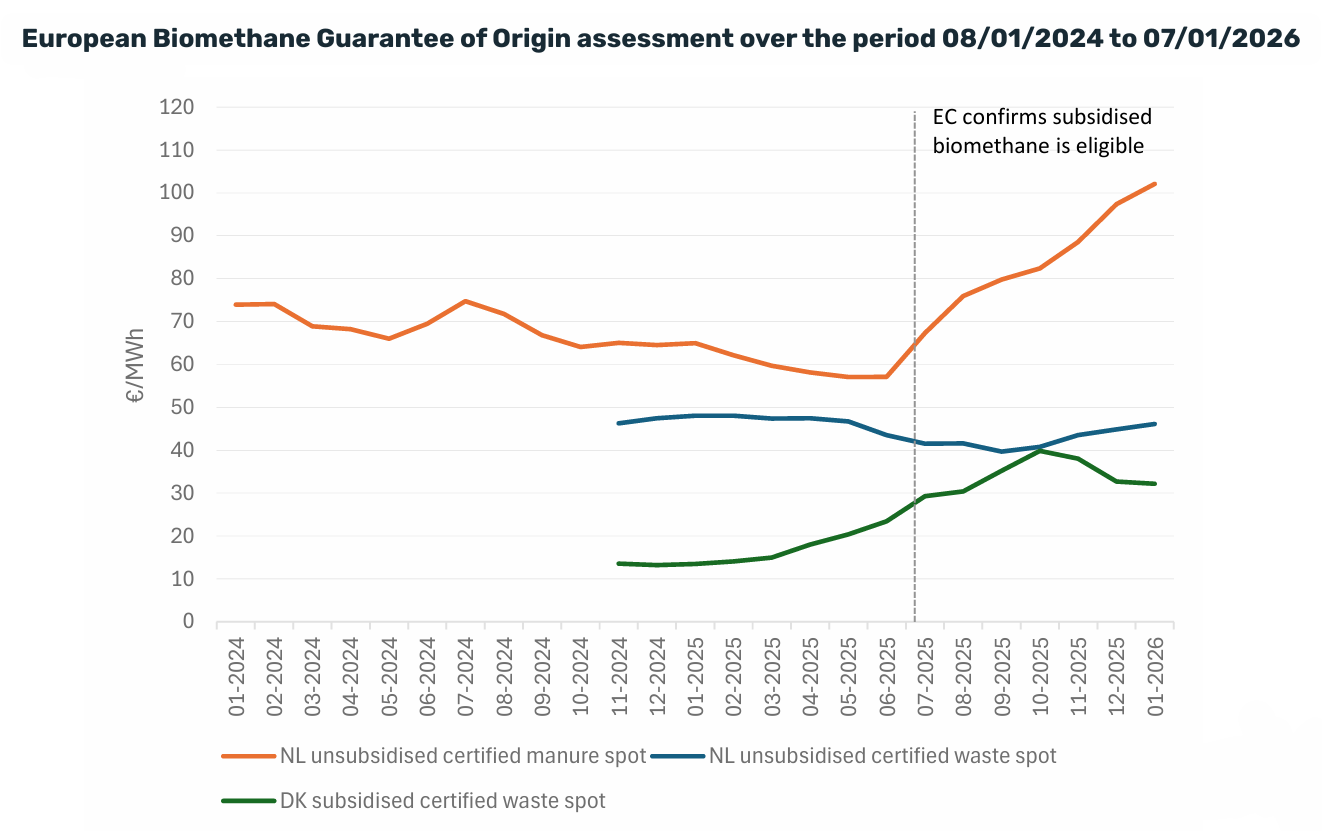

Following the European Commission’s confirmation in July 2025 that subsidized biomethane is eligible under FuelEU Maritime, prices for guarantees of origin (GO) have risen sharply. This opens up a significant new market for demand, although further growth will depend on regulatory decisions.

Two competing models of industry development

The central argument of the working paper is that scaling up biomethane is complicated by the lack of a unified strategy: member states and market players are following two fundamentally different approaches.

- A producer-oriented, subsidized model: supports both biogas and biomethane through feed-in tariffs and government subsidies. Emphasizes local value creation, support for farmers, the circular economy, and high integrity. Budget costs: France has already exceeded €1 billion in support in 2024.

- A customer-oriented, market-based model: focused exclusively on biomethane, certificate trading (GO/PoS) via cross-border markets, and biomethane purchase agreements (BPA). It emphasizes cost-effectiveness, scalability, and integration into the EU’s single internal gas market.

The EU regulatory framework does not impose any particular model and allows them to coexist. In practice, this leads to inconsistencies, uneven implementation, uncertainty, and increased risks for investors and consumers, which ultimately hinders the sector’s growth.

Key unresolved issues:

The distinction between subsidized and unsubsidized biomethane: it is unclear which biomethane qualifies for various compliance markets and under what conditions. This creates a risk of overcompensation (“double subsidization”), as confirmed by the Landwärme case, in which the European Commission annulled the Swedish support scheme.

Mass balance and the link between certificates and physical gas flows: once fed into the grid, biomethane cannot be distinguished from natural gas. The Netherlands requires physical separation for imported bio-LNG, while Germany, France, Spain, and the European Commission allow the mass balance method (“virtual liquefaction”). This dispute risks complicating cross-border trade and reducing investment attractiveness.

Conclusions and Outlook

The author highlights the following key points:

- The target of 35 billion cubic meters by 2030 is unlikely to be met in its original form — even if national plans are fully implemented.

- No technological breakthrough is expected by 2030; progress will be limited to gradual improvements in the efficiency of existing technologies.

- A decline in natural gas prices could further undermine the competitiveness of biomethane and increase pressure on support schemes.

- FuelEU Maritime is the most promising new source of demand, but its further development depends on regulatory certainty.

- Resolving the issues surrounding subsidies and mass balance is critical to the coordinated development of the EU biomethane market.