Calculation of obligations for surrender of CBAM certificates for imported goods in the EU

Under CBAM, during its final (post-transition) period starting on 1 January 2026, EU-authorised declarants representing importers of certain goods will purchase and surrender CBAM certificates for the embedded emissions of their imported goods.

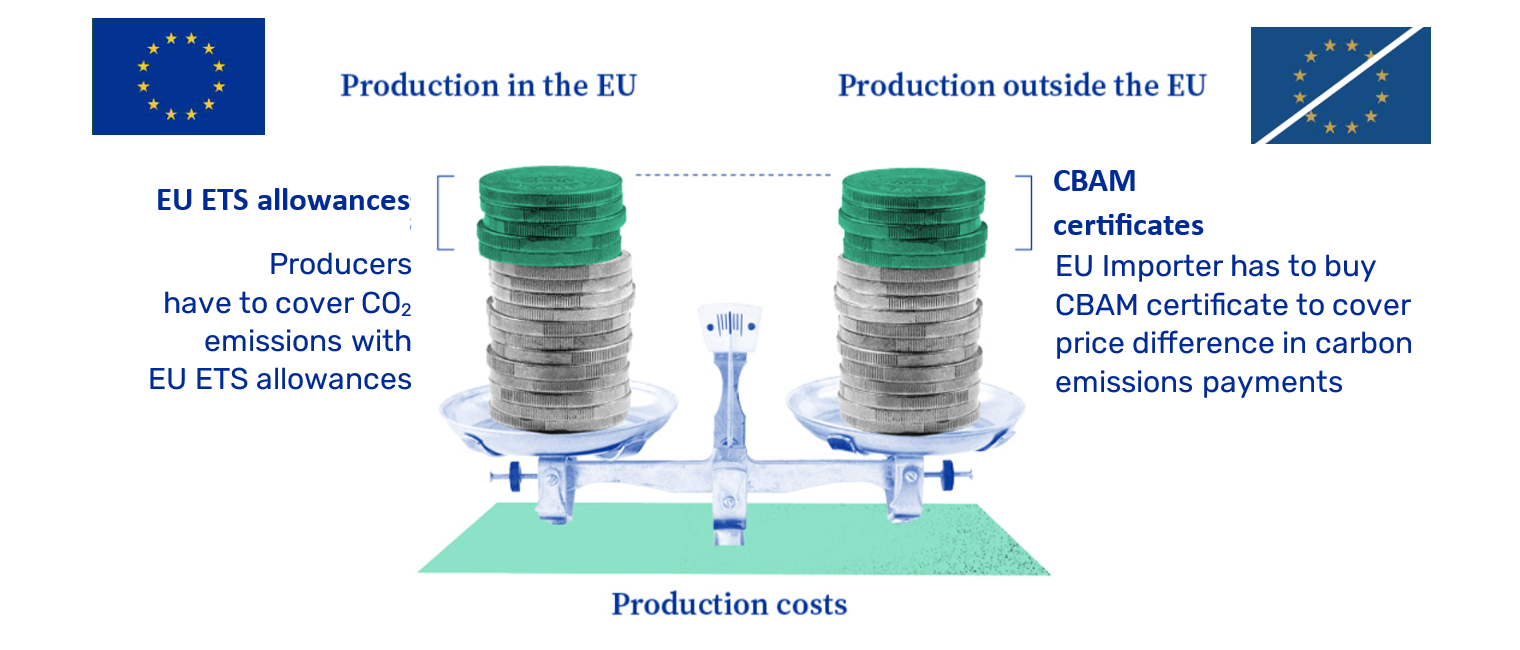

This approach will equalise the price of carbon emissions between imported goods and goods produced in installations participating in the EU Emissions Trading System (EU ETS).

By reducing the risk of carbon leakage, CBAM ensures fair treatment of goods produced in different installations in different jurisdictions.

The Carbon Border Adjustment Mechanism (CBAM) is an environmental policy instrument of the European Union designed to apply the same carbon costs to imported products as would be incurred by installations operating in the EU. In doing so, the CBAM reduces the risk of the EU’s climate objectives being undermined by production relocating to countries with less ambitious decarbonisation policies (so-called ‘carbon leakage’).

The updated version of the CBAM Q&A document of 18 December 2024, provides new information on the functioning of this mechanism in the post-transition period and the determination of the financial obligations of importers in the EU. In particular, a description of the calculation of the number of CBAM certificates that authorized CBAM declarants will need to surrender for the embedded emissions of their imported goods into the EU has been added.

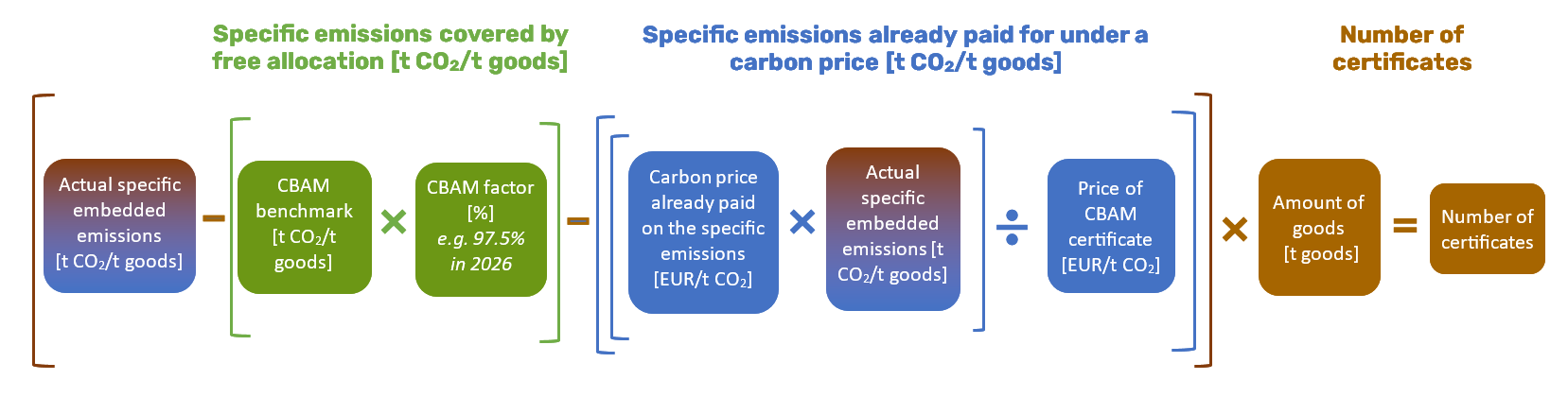

The formula for this calculation takes into account that the actual specific embedded emissions in the imported goods are subtracted from the specific emissions covered by the free allocation of the EU Emissions Trading System (EU ETS) and the specific emissions for which they have already paid in the country of origin of the goods. Thus, the number of CBAM certificates to surrender is equal to the multiplication of the specific emission cost that needs to be paid by the number of goods imported into the EU.

Let’s consider the components of this formula in more detail:

Actual specific embedded emissions:

- the installation operator outside the EU must provide the authorised CBAM declarant with data on the actual specific embedded emissions of the product and the carbon price already paid for the specific emissions.

CBAM benchmark:

- will be based on a combination of the EU ETS benchmarks;

- the CBAM benchmarks are not necessarily fixed numbers, as in some cases installation-specific data might be required.;

- while in some cases there could be a CBAM benchmark per CN code, it may also be possible that CBAM benchmarks are set per groups of CN codes (e.g. per aggregated goods category), if the respective production processes are similar. On the other hand, there could also be different CBAM benchmarks for the same CN code, for example in the case of goods made of primary versus secondary steel;

- the overall objective is to develop a methodology that mirrors the EU ETS free allocation rules while limiting the burden for stakeholders.

CBAM factor:

- rules for the adjustment for free allocation will be developed by the European Commission following the empowerment of Article 31 (2) of the CBAM Regulation;

- the CBAM obligation to be paid by importers will be reduced by the corresponding free allocation that an EU producer would receive for the production of the same goods. This will ensure that products produced in the EU and in third countries are treated equally;

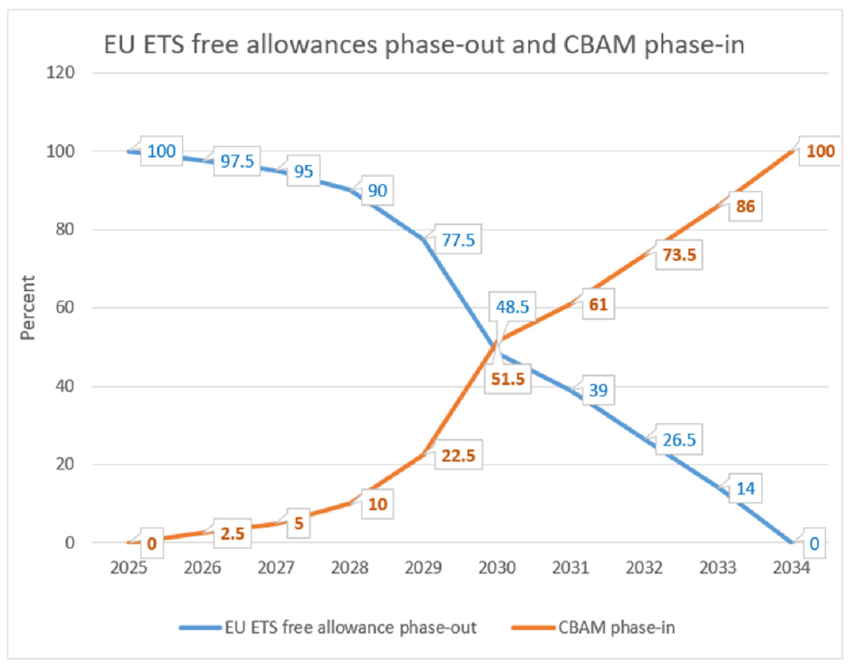

- the gradual phase-out of ETS-free allowances in CBAM sectors from 2026 to 2034 will be mirrored by a corresponding increase in the CBAM obligation. This is because the CBAM adjustment for free allocation will gradually decrease and thereby the CBAM obligation will increase.

The figure shows the schedule for the phase-out of free EU ETS allowances and the phase-in of CBAM obligations. Thus, in 2026, the CBAM obligation is 2.5%, with a CBAM factor of 97.5%.

Carbon price already paid

on the specific emissions:

- an authorised CBAM declarant can claim a reduction in the number of CBAM certificates to be surrendered corresponding to the carbon price already effectively paid in the country of origin for the declared embedded emissions of CBAM goods;

- the CBAM Regulation defines a ‘carbon price’ as the “monetary amount paid in a third country, under a carbon emissions reduction scheme, in the form of a tax, levy or fee or in the form of allowance under a greenhouse gas emissions trading system (…)”.

- only the carbon price that has been “effectively paid in the country of origin” will count for a reduction of the number of CBAM certificates. Should the authorised CBAM declarant benefit from any rebate or other form of compensation, the benefit will be the carbon price effectively paid. This would for example be the case if free allowances under an ETS are granted.

- the Commission will prepare, before the end of the transition period in 2025, an implementing act setting out additional details for the deduction of the carbon price effectively paid in the country of origin (see Article 9(4) of the CBAM Regulation).

Price of CBAM certificate:

- the Commission will calculate the price of CBAM certificates on a weekly basis, as the average of the closing prices of EU ETS allowances on the auction platform. This price will be calculated in EUR and made publicly available. Each CBAM certificate will correspond to one tonne of CO2 equivalents emitted.

Number of certificates:

- the amount of declared CBAM goods imported into the EU is expressed in metric tons.

Purchase of CBAM certificates

Authorised CBAM declarants will buy CBAM certificates from the Member State where they are established. All purchases will take place on the common central platform which the Commission will establish. Only authorised CBAM declarants will be allowed to purchase CBAM certificates at any time throughout the year.

However, authorised CBAM declarants will have to buy a number of CBAM certificates which corresponds to at least 80% of the emissions embedded in the CBAM goods that they have imported into the EU since the start of the year. This rule will be calculated on a quarterly basis, which means that declarants will have to ensure they meet this requirement at the end of each quarter of each calendar year (31 March, 30 June, 31 October and 31 December).

The status of CBAM Authorized Declarant is granted by the National Competent Authority of CBAM in the EU Member State in which the applicant is registered. The following criteria must be met:

- has not been involved in a serious infringement or in repeated infringements of customs legislation, taxation rules, market abuse rules or the CBAM Regulation;

- demonstrates its financial and operational capacity;

- is established in the Member State where the application has been submitted;

- has been assigned an EORI number.

Surrender of CBAM certificates

First, authorised CBAM declarants will submit their annual declaration in the CBAM registry by 31 May each year and for the first time by 31 May 2027 for the year 2026. The annual declaration will indicate the number of CBAM certificates that they will have to surrender. This number of CBAM certificates to be surrendered corresponds to the amount of embedded emissions, expressed in tons of CO2, of the CBAM goods imported into the EU during the year covered by the annual declaration.

Second, by 31 May each year and for the first time by 31 May 2027 for the year 2026, authorised CBAM declarants will surrender the number of CBAM certificates, in the CBAM registry, which they have declared in their annual declaration for the same year. To do so, authorised declarants will select the certificates that they want to surrender among the CBAM certificates which are available in their CBAM account in the registry.

The procedures described directly affect importers of goods under CBAM. However, manufacturers of goods exported to the EU must also take into account the new CBAM requirements and take measures to reduce the specific embedded emissions of their products in order to remain competitive in the European market. Namely, the value of the actual specific embedded emissions of CBAM goods determines the size of the financial obligations of importers in the EU.

The publication was prepared within the framework of the project “Technical Assistance for CBAM good exports from UA to EU“, which is implemented with the support of the Ministry of Foreign Affairs of the Kingdom of the Netherlands and the Netherlands Enterprise Agency. Funding is provided by the Private Sector Development Program of the Netherlands Enterprise Agency/The Netherlands Enterprise Agency.

The project “Technical Assistance for CBAM good exports from UA to EU” began on November 25, 2024, and will last until February 28, 2026. This project is implemented with the support of the Ministry of Foreign Affairs of the Kingdom of the Netherlands and the Netherlands Enterprise Agency.