CBAM Regulatory Framework for the Definitive Period Starting in 2026

Starting from January 1, 2026, the European Union’s Carbon Border Adjustment Mechanism (CBAM)is moving from a Transitional to a Definitive period.

This means that importers of certain goods will not only have to report their greenhouse gas emissions, as has been the case since October 2023, but will also have to buy and surrender certificates for those emissions.

Thus, the greenhouse gas emissions embedded in goods imported into the EU will become a real operational cost.

Non-EU producers and exporters whose products fall under the CBAM have just a few months left to prepare for the definitive period, which will commence in 2026. There are currently many uncertainties, as amendments to the CBAM regulation are still being finalised, and several legislative acts are in the pipeline.

To calculate the costs of CBAM, which are necessary for business planning and signing long-term contracts, four key elements are particularly important for businesses:

- Benchmarks: These will determine how many CBAM certificates importers must submit. Until these are published, the real values of imports in 2026 will remain unknown.

- Verification rules: Companies need to know how emissions data will be verified and which verifiers will be recognised.

- Default values: Some importers will have to use default values if data from the supplier is not available. The size of the “mark-up” to these values is not yet known, which makes it difficult to assess financial risks.

- Certificate purchase rules: A clear certificate purchase schedule is important for cash flow planning and avoiding disruptions.

Companies are working hard to prepare, but the lack of clear guidance leaves them vulnerable. Goods ordered today will arrive in 2026 and will be subject to CBAM, but companies still lack an understanding of how much tax they will have to pay.

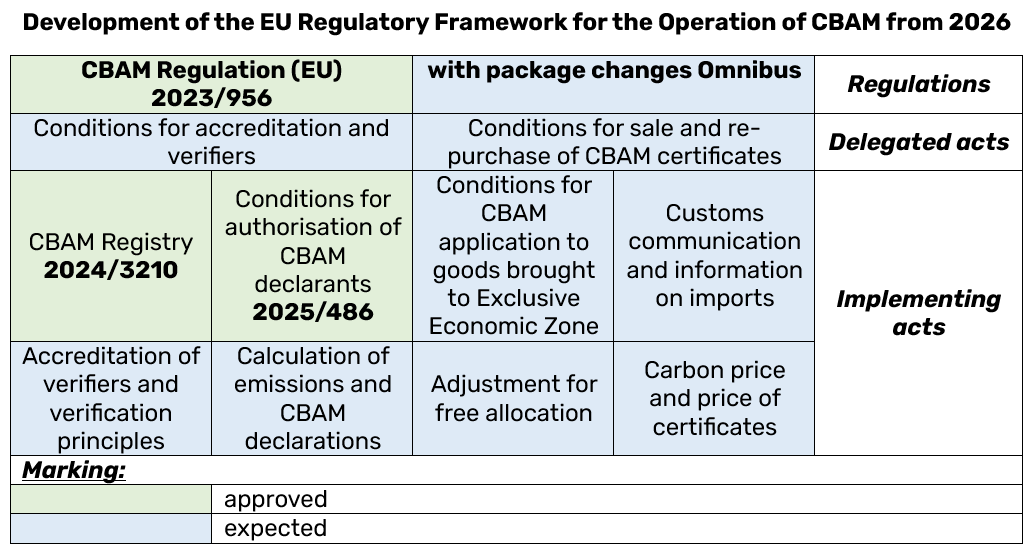

Consider the overview of 10 delegated and implementing acts prepared by CO2iq Solutions GmbH, which define how CBAM will operate from 2026. To date, only two of these acts have been adopted, while the rest are at various stages of development, and some are even delayed compared to the original schedules. These documents detail the rules in three main areas, which are critical for the operational readiness of the finance, procurement and customs departments of importing companies.

From August 28 to September 25, the European Commission announced the call for applications for the methodological framework for the definitive period of the CBAM, which includes:

- determination of the direct embedded emissions based on actual emissions;

- determination of embedded emissions for electricity;

- determination of indirect embedded emissions;

- default values for non-electricity goods that will be used if the embedded emissions are not based on actual data.

Currently, a transition period is in effect until the end of 2025, during which the implementing regulation CBAM 2023/1773, which regulates quarterly reporting by importers, is in effect.

To simplify CBAM and facilitate its compliance, in February 2025, the European Commission proposed several amendments to the main CBAM Regulation (EU) 2023/956 in the Omnibus package, which were described in detail in our publications:

Simplification of CBAM for importers and operators of installations outside the EU: part one

Simplification of CBAM for importers and operators of installations outside the EU: part two

On September 10, the European Parliament officially voted in favour of the agreed simplifications of the Omnibus package. After formal approval by the Council of the European Union, these changes will be reflected in the relevant EU regulatory documents.

Overview of delegated and implementing acts in three areas of application

CBAM Permits and Customs Regulations

From 2026, goods subject to CBAM can only be imported into the EU by authorised CBAM declarants. Importers must apply for an authorisation.

Following a public consultation, Implementing Regulation 2025/486 was published in March 2025. Applications opened on 31 March 2025.

Additional customs rules are being developed, including import data transmission requirements. Draft rules for goods entering the exclusive economic zone of member states were published in July 2025.

CBAM emissions and their verification

Even during the current transition phase, importers are required to report actual emissions from the production of CBAM goods using CBAM methods. However, there is currently no formal mechanism to ensure that the data meets these standards.

From 2026, only verified emissions data confirmed by CBAM-accredited verifiers will be accepted.

National accreditation bodies will approve verifiers in accordance with the conditions set out in a delegated act. A separate implementing act will define the principles of verification and the required qualifications. Both acts, initially planned for Q4 2024, have been postponed.

Verifiers will be responsible for:

- Verification of emission monitoring and calculation methods.

- Conducting inspections of production facilities.

- Issuance of verification reports to manufacturers.

If verified data is not available, importers must use national default values with a markup that increases the cost. Both of these elements have yet to be finalised.

The rules for calculating emissions from 2026 will be set out in a new implementing regulation, expected in Q4 2025. It will define:

- How to calculate direct emissions.

- Whether and how to include indirect emissions.

- What default values are applied if actual data is not provided.

- How to account for emissions related to electricity.

CBAM certificates and their calculation

From 2026, importers will be required to purchase CBAM certificates to include emissions in their products.

The number of certificates will be adjusted to take into account:

- The level of free allowances granted to EU producers.

- Carbon prices already paid in the country of origin.

These two factors are key to calculating CBAM costs. Implementing acts regulating both items is expected in Q4 2025.

Importers should only purchase certificates for emissions exceeding a certain benchmark, based on EU production standards and adjusted using the CBAM factor. The implementing act will specify how these benchmarks are calculated for specific products.

Another implementing act will determine how to convert carbon prices paid abroad into the number of CBAM certificates, as well as how to estimate actual payments. It is also expected that this act will determine which carbon prices can be counted towards CBAM.

Only authorised declarants can buy CBAM certificates, which will be traded via the EU Central Platform. The rules for buying, selling and returning certificates will be set out in a delegated act, which has not yet been adopted.

This platform is accessed through the CBAM Register, the rules for which were published in Implementing Regulation 2024/3210.

Conclusions

With the transition to a definitive period in 2026, CBAM will transform from an administrative requirement into an important strategic and financial factor for all companies importing products into the EU. Ignoring these changes can lead to serious consequences: from significant financial losses and delays in delivery to loss of market positions.

Although the regulatory framework for the definitive CBAM period is still being developed, and there is no solid data to accurately estimate additional costs, Ukrainian manufacturers of goods subject to the mechanism need to act now. They should not only create a reliable system for monitoring and calculating greenhouse gas emissions, but also develop and implement emission reduction measures. This is what will give them a competitive advantage in the EU market in the future.

The publication was prepared within the framework of the project “Technical Assistance for CBAM good exports from UA to EU“, which is implemented with the support of the Ministry of Foreign Affairs of the Kingdom of the Netherlands and the Netherlands Enterprise Agency. Funding is provided by the Private Sector Development Program of the Netherlands Enterprise Agency/The Netherlands Enterprise Agency.

The project “Technical Assistance for CBAM good exports from UA to EU” began on November 25, 2024, and will last until February 28, 2026. This project is implemented with the support of the Ministry of Foreign Affairs of the Kingdom of the Netherlands and the Netherlands Enterprise Agency.